We have launched E-mail Alert service,subscribers can receive the latest catalogues free of charge

Analysis of and Policy Options on Further Opening of China's Insurance Market

Dec 09,2008

Zhang Chenghui, Chen Daofu, Lei Wei & Tian Hui

I. The Opening up of China's Insurance Market

1. Relevant provisions of opening policies (1) Opening policy on market access to foreign institutions When joining the World Trade Organization (WTO), China made commitments in five areas including form of incorporation, geographic scope, business scope, business license issuance and mandatory insurance. They cover the following aspects.

Foreign life insurance companies would be allowed to establish business institutions in China in the form of joint-venture companies but would not be allowed to have more than 50% equity holding; foreign non-life insurance companies would be allowed to establish branches, joint-venture companies and wholly-owned subsidiary companies.

—The geographic restriction, which had limited foreign insurance companies to Shanghai, Guangzhou, Dalian, Shenzhen and Fushan before China's WTO accession, was lifted. With approval, foreign insurance companies would be allowed to establish subsidiaries in any part of China.

—With regard to business scope, foreign life insurance companies, which had been limited to operating life insurance business for foreigners and for Chinese who personally paid premiums, would be allowed to provide personal life insurance service, health insurance, group insurance and pension/annuity service to both Chinese and foreign customers. Foreign non-life insurance companies, which had been limited to operating property insurance business for overseas enterprises and operating property insurance and related liability insurance, credit insurance, master policy and major commercial insurance for foreign-invested enterprises in China, would be allowed to operate all insurance businesses except mandatory insurance lines (third-party liability insurance for motor vehicles and liability insurance for the drivers and carriers of commercial transport vehicles).

—Foreign reinsurance companies would be subject to neither the restriction on the form of incorporation nor the restriction on geographic location and the restriction on the number of business licenses.

—With regard to the conditions of incorporation, foreign insurance institutions would enjoy full national citizen treatment in capital requirement. But an insurance brokerage company must have US$200 million in total assets, higher than the 10-million-yuan paid-up capital required for a Chinese company.

—With regard to the qualification of foreign shareholders, they would have to meet the requirements of total assets and business history (a shareholder must have operated insurance business for more than 30 years, its total assets at the end of the year before incorporation application should not be less than US$5 billion, and the applicant has had a representative office in China for more than two years). The insurance industry has the same requirement for foreign capital participation in Chinese insurance companies as the banking industry does, namely the investment in a Chinese financial institution by a single overseas financial institution should not exceed 20% and the total shareholding by foreign capital should not exceed 25%.

—The 20% mandatory ceding to a Chinese reinsurance company at the time when China joined the WTO would be lifted.

(2) Opening policy on the control of operational activities of insurance companies

With regard to the control over the operational activities of insurance companies, foreign companies are currently enjoying the same national citizen treatment as Chinese companies do. There is no differential policy in this respect. Specifically:

—Product development and pricing1. In property insurance, the basic terms and premium rates of major commercial insurance types are no longer set by China Insurance Regulatory Commission. The Insurance Association of China has been authorized to set the insurance terms, model texts and guiding premium rates. The China Insurance Regulatory Commission is only in charge of examining and approving the terms and premium rates of mandatory insurance, guaranteed insurance with a period of more than one year, and credit insurance. Other product lines are only required to report to the commission for the record. In life insurance, the assumed interest rate is still limited to 2.5% or lower.

—Investment and assets management. China Insurance Regulatory Commission has accelerated the exploration of more channels for insurance investments since 2004. On the basis of allowing insurance funds to invest in bank deposits, treasury bonds and financial bonds, the commission also allowed insurance funds to invest in corporate bonds, securities investment funds and directly invest in stock markets, overseas stock markets and equities of domestic commercial banks. Later on, it raised the ratio of investing insurance assets in stock markets from 5% to 10% of the total assets, allowed insurance companies to use 15% of their total assets for overseas investment, and expanded the scope of overseas investment from the fixed-earning category to shares, stock rights and other equity products. In the meantime, the commission established a relatively high threshold for high-risk investment and encouraged small- and medium-sized insurance companies to carry out entrusted investment through the assets management companies established by major insurance companies. Currently, most small- and medium-sized insurance companies have no qualification for direct stock investment except nine Chinese-invested insurance assets management companies and the specially-approved Asset Management Center of China Region of American International Assurance Co., Ltd. For overseas investment, an insurance company must have at least 10 billion yuan in total assets and therefore small- and medium-sized insurance companies, both Chinese and foreign, are difficult to acquire this qualification.

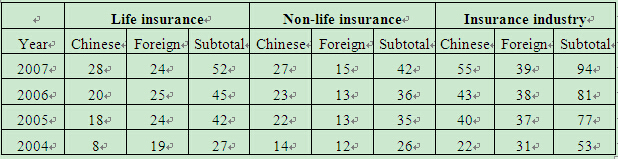

—Capital regulation. In January 2001, China Insurance Regulatory Commission promulgated the Interim Regulations on the Administration of the Minimum Solvency and Regulatory Indicators of Insurance Companies, thus beginning an experiment on solvency regulation, which used the relatively simple, EU-type fixed ratio model, instead of the risk capital method. 2. State of foreign capital operations after China opened insurance market (1) Foreign capital participation in China's insurance industry Foreign capital participation in China's insurance industry was mainly done in three forms: branch companies, Sino-foreign joint-venture companies and strategic investors' participation. In addition, some foreign capital enjoyed the development fruit of China's insurance industry by holding the overseas-listed stocks of Chinese insurance companies. By the end of March 2008, a total of 49 foreign insurance companies from 15 countries and regions across the world had established a total of 161 business institutions in China (including those under preparation). Table 1 shows the numbers of Chinese and foreign insurance companies formally operating in China's insurance market during the 2004~2007 periods. It indicates that foreign insurance companies account for nearly 50% of the total number of insurance companies.

Table 1 Numbers of Chinese & Foreign Insurance Companies Formally Operating in China's Insurance Market